Cost reporting tracks construction spending against budget. Learn how to build clear cost reports, avoid mistakes, and keep projects on budget.

Use this FREE Project Cost Report Template to track, analyze, and communicate your project’s financial performance. Compare budgeted, committed, and actual costs to stay on top of your budget.

Cost reporting provides stakeholders with detailed insights into the financial health of the project, ensuring costs are kept in check while work progresses. But what exactly does cost reporting entail, and why is it so crucial in the construction industry?

Let’s talk about what cost reporting is and break down its key components. Learn why mastering it is fundamental for successful project delivery.

Cost reporting is the practice of tracking and communicating the financial performance of a construction project. A construction cost report consolidates information on expenses, budgets, and forecasts, helping project managers make informed decisions. It covers every aspect of project spending, from labor costs and materials to overhead.

For example, imagine you’re managing a $10 million construction project. Without a clear view of your spending, it’s easy to lose sight of how much has been allocated, spent, or set aside for unforeseen expenses. A cost report gives you that visibility in real time.

By consistently updating and reviewing cost reports, project managers can prevent cost overruns, mitigate financial risks, and ensure that the project remains on budget.

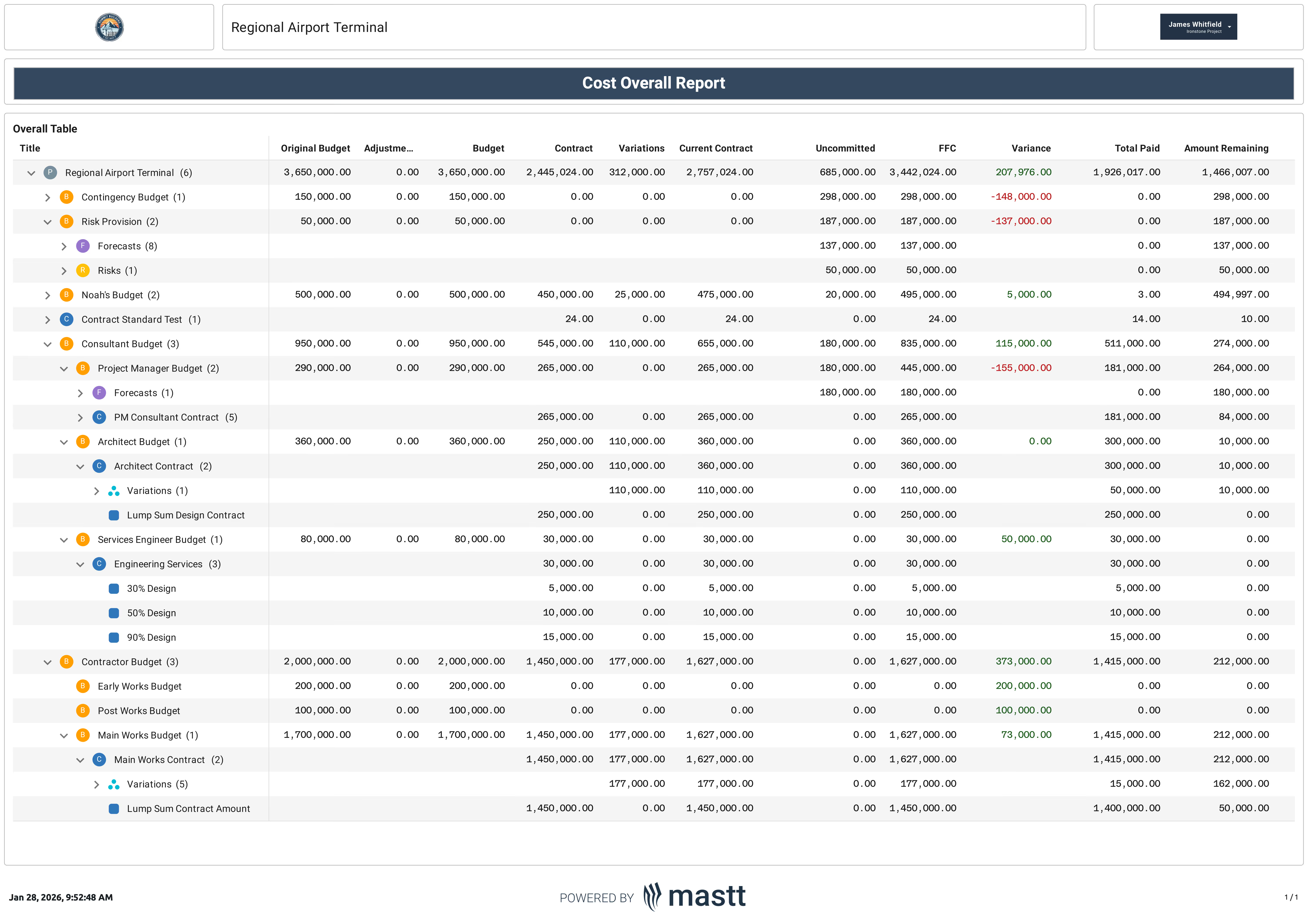

A good cost report example shows a project's budget, expenses, and financial status clearly. Below is a construction cost report, breaking down costs, additional expenses, and project progress. This helps teams track spending, stay on budget, and make smart decisions.

Cost reporting is built on five core aspects, including budget tracking, forecasting, and cash flow projections. Each element plays a specific role, but cost reporting only works when all five stay aligned throughout the project.

Effective cost reporting typically involves the following elements:

Project budget tracking is monitoring how much has been spent versus the allocated budget. It shows how much money has been allocated, spent, and committed for each scope of work. Accurate construction cost tracking depends on a stable baseline and consistent updates as contracts and changes are approved.

For example, if you’ve allocated $100,000 for materials but have already spent $80,000, you can quickly adjust to stay within budget. Budget tracking prevents unpleasant surprises and keeps your project financially stable.

Forecasting is the process of estimating future costs based on current trends and project progress. It looks ahead, helping you predict costs based on current trends. A reliable forecast changes when conditions change, not only after costs are fully spent.

Imagine your project is halfway through, and you’ve spent 60% of the budget. Construction cost forecasting helps you understand whether you need to cut back or secure additional funds to finish the project on time.

Change orders are the adjustments to the project scope that impact the overall budget. Change order management captures how these scope changes affect the project budget. Approved changes update the cost report, while pending changes signal potential exposure.

For instance, if the client requests a larger conference room, the additional costs are captured in a change order. This way, your cost report stays accurate and up-to-date.

Variance analysis helps you identify differences between what you planned to spend and what you actually spent. If your labor costs are higher due to overtime, variance analysis pinpoints this issue. You can then adjust schedules or hiring plans to control costs.

Cash flow projections estimate when funds will be required to keep the project moving smoothly. They help owners plan funding and help contractors manage billing and payments. Cash flow accuracy depends on aligning cost data with the project schedule.

For example, if you’re waiting on a client payment but have supplier invoices due, cash flow projections help you prepare and avoid delays.

A construction cost report pulls together the financial data needed to track budget performance and expected final cost. It shows where the project stands today and whether costs are trending over or under the approved budget.

Actual and committed costs show what has already happened, while forecasts and pending changes highlight future exposure. Clear notes and assumptions explain why numbers are moving, and help owners understand whether cost pressure comes from scope changes, market conditions, or execution.

Cost reporting gives project teams a clear view of financial performance while there is still time to respond. It turns raw cost data into usable information that supports day-to-day decisions and long-term budget control.

Timely, accurate cost reporting enables project teams to:

✅ Keep stakeholders informed

Stakeholders need to know how their money is being spent. Cost reporting provides the transparency they expect. It shows them that the project is financially on track or highlights where adjustments are needed.

Imagine presenting a report that clearly outlines your budget, current spending, and future projections. It builds trust and confidence among clients, investors, and your own team. Nobody likes surprises when it comes to finances, and regular cost reports help prevent them.

✅ Control costs proactively

Cost reporting flags potential problems before they turn into full-blown crises. For example, if labor costs are trending higher than planned, a timely report allows you to act. You can adjust schedules, negotiate better rates, or find other ways to stay within budget.

Cost reporting helps you spot risks and take corrective action while there’s still time to fix them.

✅ Optimize resource allocation

Construction projects are complex, with many moving parts. Cost reporting helps you see where resources are being used most effectively. It also shows where adjustments are needed. By reviewing expenditure, project managers can reallocate resources efficiently to avoid bottlenecks.

✅ Improved forecast accuracy over time

Regular cost reporting improves forecast quality by forcing updates based on current conditions. Forecasts that evolve with real data are far more reliable than static estimates created early in the project. Over time, this leads to fewer surprises late in construction.

Cost reporting matters because it connects financial data to real project behavior. When teams treat it as a management tool instead of a reporting task, it becomes easier to spot risk, explain cost movement, and keep the project aligned with financial expectations.

To run effective cost reporting, start by establishing a clear structure for tracking, updating, and reviewing costs. Strong cost reporting depends less on tools and more on disciplined processes that stay consistent from day one.

Establish a realistic budget at the beginning of the project, considering potential risks and cost changes. Look at every detail of your project, from materials to labor, and don’t forget to account for risks like delays or price changes. A solid baseline gives you something to measure against as the project moves forward.

Cost reporting works best when budgets, contracts, and invoices all use the same cost codes. Misaligned codes force manual adjustments and weaken report accuracy. Keep the structure simple enough to maintain, but detailed enough to track meaningful scope.

Don’t wait until the end of the project to figure out where the money went. Use project cost management software for construction to update reports in real-time as the project progresses. This way, you can see how your spending matches up with your budget at every stage.

Budget variances are inevitable. These are the differences between what you planned to spend and what you actually spent. The key is to catch them early and understand why they happened. Analyze any differences between budgeted and actual costs to determine if corrective actions are needed.

Cost reporting isn’t a solo effort. Involve all key stakeholders in regular cost review meetings. Open communication ensures everyone understands the project’s financial health and can contribute to finding solutions when needed.

💡Pro Tip: Assign one owner to approve forecast changes and one cutoff date for each reporting period. Multiple versions of the truth usually start with multiple people updating the forecast at different times.

Cost reporting is a shared responsibility, but it works only when roles are clearly defined. Each party contributes different inputs, and breakdowns usually happen when ownership is assumed rather than assigned.

While many teams contribute data, cost reporting fails when no single person owns the forecast and variance explanations. Clear ownership ensures issues are addressed early instead of debated after the fact.

Most cost reporting problems come from process gaps. When these issues repeat, reports lose credibility and stop supporting real decisions.

These mistakes tend to compound. Late updates weaken forecasts. Blended costs hide scope growth. Missing explanations turn reports into static documents instead of working tools. Fixing even one of these issues usually improves reporting quality fast.

Effective cost reporting is built on habits and systems that keep financial data accurate, consistent, and useful for real decisions. The following practices reflect how successful teams maintain control over project costs and communicate clearly with stakeholders.

☑️ Use automated tools

Replace manual spreadsheets with cost report software that collect and display cost data in real time. Automation reduces errors, speeds up reporting, and gives immediate access to budgets, actuals, and forecasts.

Modern construction project management software, like Mastt, consolidates data from contracts, invoices, and purchase orders. This reduces time spent reconciling numbers and allows teams to focus on acting on insights.

☑️ Incorporate historical data

Historical project cost information helps refine forecasts and reveals patterns in overspending or risk areas. When teams compare current cost trends to past performance, they can better predict budget pressure points and adjust plans early. This reduces surprise variances later in the project cycle.

☑️ Maintain regular reporting intervals

Update cost reports frequently to keep the information current. Stale data hides emerging issues and weakens decision-making. Daily or weekly updates on key cost metrics ensure every stakeholder sees up-to-date financial status and can react before problems grow.

☑️ Foster cross-functional collaboration

Bring finance, procurement, and project teams together when preparing cost reports. Shared understanding of cost drivers and data sources improves accuracy and speeds reconciliation. Collaboration prevents siloed reporting and builds trust across teams.

☑️ Standardize reporting formats

Use consistent a cost reporting template and structures for all cost reports. Standardized formats make it easier to compare reports across periods and projects, reduce confusion, and ensure key data points are always included. Teams that speak the same reporting language make faster, more confident decisions.

💡Pro Tip: Tie automated reporting tools to your accounting or ERP system so committed and actual cost data sync in real time. This eliminates manual entry errors and ensures forecasts reflect the most current financial picture.

Project teams rely on a mix of systems to track costs, maintain forecasts, and communicate financial status. The right toolset depends on project size, reporting complexity, and the number of stakeholders that need access to the data.

Most projects use several tools, but cost reports break down when those tools fall out of sync. When budgets, commitments, and forecasts are stored in different systems, teams spend time reconciling numbers rather than keeping cost data current. Closing those gaps requires better-connected systems.

Cost reporting tools with AI capabilities supports cost reporting by keeping data aligned, flagging changes early, and reducing manual effort. Instead of relying on static reports, project teams work with live cost information that reflects current project conditions.

🤖 Centralizing and interpreting cost data

AI-powered software, like Mastt, brings budgets, commitments, actuals, and forecasts into one system and continuously interprets how those figures relate to each other. This reduces reliance on spreadsheets and manual checks. Teams see a clearer financial picture without stitching data together.

🤖 Improving forecast accuracy

AI helps identify patterns in cost movement and highlights when forecasts no longer match project reality. Instead of waiting for overruns to appear in totals, teams get early signals that assumptions need review. Forecasting becomes more responsive and less reactive.

🤖 Reducing human error in reporting

Automation paired with AI logic limits calculation errors, missed updates, and version conflicts. Rules are applied consistently across reports, even as data changes. This improves trust in the numbers being shared with owners and stakeholders.

🤖 Increasing insight for decision-making

AI-powered dashboards surface trends, variances, and exposure without requiring teams to dig through line items. Owners and project managers can focus on what changed and why. Tools like Mastt apply AI in this way to support clearer, faster cost conversations.

🤖 Supporting scalable and consistent reporting

As project portfolios grow, AI-powered construction project management software helps teams apply a consistent cost reporting structure across multiple projects without adding administrative work. This consistency makes it easier to compare performance and spot emerging cost risk.

Software does not replace judgment. It supports it by removing manual friction and keeping reports aligned with current conditions. Cost reporting still requires ownership, review, and explanation.

Colliers’ project leaders struggled to deliver timely and consistent cost reports as their project portfolio grew. Cost data was spread across spreadsheets, PDFs, and separate documents, requiring manual consolidation for every reporting cycle. The process was slow and increased the risk of inconsistencies reaching clients.

Moving to a centralized reporting platform

To address these issues, Colliers adopted Mastt to centralize budgets, commitments, invoices, and forecasts in one system. With cost data connected and continuously updated, reports and dashboards reflected current project conditions without manual rework. Mastt replaced fragmented files with a single source of truth.

Clearer visibility for project teams and clients

The new approach gave Colliers real-time visibility into project costs. Automated dashboards showed current budget status, forecast movement, and exposure in a clear, consistent way. Project teams and clients could review financial performance without waiting for static files to be compiled and checked.

Results: Accuracy, speed, and trust

With centralized and AI-supported cost reporting, Colliers reduced reporting effort and improved accuracy. Teams shifted focus from compiling numbers to explaining variances and supporting decisions.

Clients received clearer insight into project finances, which strengthened confidence and improved the quality of cost conversations. As a result, Colliers expanded the use of Mastt across additional projects.

Cost reporting plays a central role in keeping construction projects financially controlled and predictable. When done well, it gives project teams early visibility into cost risk, supports better decisions, and creates transparency for owners and stakeholders.

Effective cost reporting depends on consistent processes and reliable systems. By applying proven practices and using software like Mastt to centralize cost data and reduce manual work, cost reporting becomes a practical tool for managing projects.

Written by

Jackson Row is the Growth & North American Market Lead at Mastt. With a background in risk modeling, cost forecasting, and integrated project delivery, he helps capital project owners work smarter and faster. Jackson’s work supports better tools, better data, and better outcomes across the construction industry.

Contributions from

Cut the stress of showing up unprepared

Start for FreeTrusted by the bold, the brave, and the brilliant to deliver the future

![What to Include in a Construction Cost Report [Examples]](https://cdn.prod.website-files.com/607f739c92f9cf647516b37b/673325cfc0431e0bcb96cbb8_66fa6b3e729571b2ca1ef55d_What%2520to%2520Include%2520in%2520a%2520Construction%2520Cost%2520Report.avif)

![What to Include in a Construction Cost Report [Examples]](https://cdn.prod.website-files.com/607f739c92f9cf647516b37b/63d87efa7c9fde41daf46741_Mastt_headshots_%20(54).avif)